Garden Grove Chemical Emergency: A Guide for Business Owners in the Evacuation Zone

By Kocaj Law · May 24, 2026

Attorney Advertising.

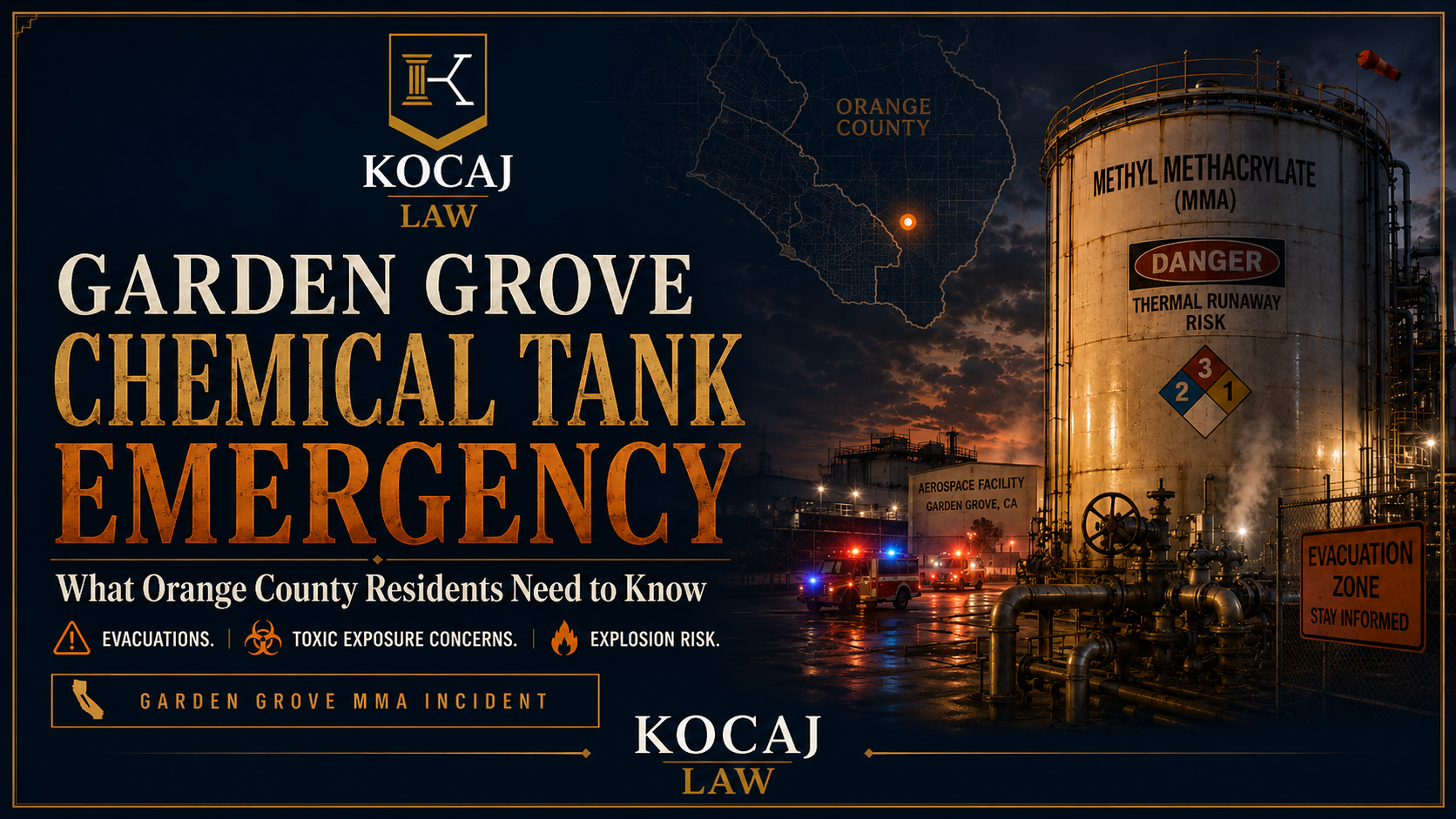

If you own or operate a business inside or adjacent to the Garden Grove evacuation zone, the chemical tank emergency at the GKN Aerospace Transparency Systems facility is not just a public safety story. It is a developing financial event for you, and the decisions you make this week will affect what you can recover later. For the broader background on the incident, see our full analysis.

Who This Applies To

Restaurants, retail shops, medical and dental offices, salons, gyms, professional services, warehouses, manufacturers, and any other business located within the mandatory evacuation footprint across Garden Grove, Cypress, Stanton, Anaheim, Buena Park, and Westminster, or close enough to it that staff or customers could not safely reach you.

The Three Buckets of Loss You Should Be Tracking

Direct closure losses. Revenue you would have earned during the days you were closed, plus payroll you still paid, perishable inventory you lost, and missed contractual deadlines.

Continuing fixed costs. Rent, utilities, insurance premiums, equipment leases, loan payments, and software subscriptions that kept running while your doors were shut.

Recovery and reopening costs. Cleaning, air-quality testing, restocking, re-marketing to customers who assumed you were permanently closed, and any temporary relocation expenses.

Insurance: Read Your Policy This Week

Most commercial property policies contain two coverages that activate during incidents like this one, and many business owners never file because they assume coverage does not apply.

Civil authority coverage typically pays business interruption losses when a government order prevents access to your premises, even if your building was never physically damaged. A mandatory evacuation order is exactly the kind of trigger this coverage was written for.

Business income coverage pays for lost net income and continuing operating expenses while your business is shut down due to a covered event. Whether the underlying event is covered depends on the policy language, and some policies exclude pollution events while others do not.

Notify your carrier in writing now, even if you are not sure coverage applies. Late notice is one of the easiest reasons for an insurer to deny a claim.

What to Document, Starting Today

- Daily revenue for the same dates over the prior two to three years (POS reports, merchant statements, tax returns).

- Payroll records for the closure period.

- Inventory loss with photographs and supplier invoices.

- All communications from city, county, and state officials regarding the evacuation order and the dates it was in effect.

- All communications with your insurance carrier, including the date and method of every notice you provided.

- Receipts for any cleaning, testing, relocation, or recovery expenses.

- Customer cancellations, missed reservations, and any contracts you could not perform.

Class Action or Individual Claim?

A class action has already been filed on behalf of two evacuees. Class actions are designed to compensate the average class member, which usually means an average household. For most businesses with meaningful interruption losses, an individual claim is the better vehicle because your damages are quantifiable, documented, and substantially larger than the average household claim.

Joining the class is not always the wrong move, but it should be a decision, not a default.

Common Mistakes to Avoid

- Signing a release or settlement offer from the facility, its insurer, or a third-party adjuster without legal review.

- Waiting until you reopen to call your insurer. Notice deadlines run from the date of the event, not the date you get around to it.

- Throwing away spoiled inventory before photographing and itemizing it.

- Assuming pollution exclusions automatically bar your claim. The case law in California is more nuanced than the policy language suggests.

- Telling customers you are permanently closed. Use social media and your website to communicate a clear reopening timeline.

Follow This Story on Social Media

We are also covering this incident on Instagram and LinkedIn.

How Kocaj Law, P.C. Can Help

We represent Orange County businesses in property damage, business interruption, toxic exposure, and insurance bad faith matters. If your business was inside the evacuation zone or otherwise impacted by the Garden Grove chemical incident, we can review your policy, evaluate your losses, and help you decide whether to pursue an individual claim, join the class action, or take a different path. Initial consultations are free, and we work on contingency for qualifying matters.

This commentary is provided for informational purposes only and does not constitute legal advice or create an attorney-client relationship. Insurance coverage is fact-specific and depends on your particular policy language.

Disclaimer: This commentary is provided for informational purposes only and does not constitute legal advice or commentary on any specific pending case. No attorney-client relationship is formed by reading this content. Past results do not guarantee future outcomes.

Free consultation

If this headline feels personal, talk with Kocaj Law before evidence disappears.

Serious freeway crashes move quickly from emergency response to insurance defense. Our firm can help preserve video, identify every responsible party, and explain your options with no upfront fee.